Ghana’s Golden Crops: The 5 Commodities Driving Africa’s Next Agricultural Trade Boom

Ghana doesn’t have an “opportunity problem". Ghana has a value-capture problem.

We grow and trade world-relevant commodities, then ship them out in raw or semi-raw form and buy back finished products at a premium.

If Ghana wants to turn agriculture into a serious engine for foreign exchange, jobs, and industrial depth, these five commodities stand out as golden crops:

Cocoa

Cashew

Oil Palm

Shea

Soybeans

Not because they’re trendy, but because the global market already pays, demand is broad, and the value chain has multiple “layers” Ghana can capture: processing, refining, fractionation, packaging, ingredients, and consumer products.

Let’s break down the numbers, the deficits, and the strategic play.

1) Cocoa: the crown jewel; now the government is pushing processing harder

Cocoa remains Ghana’s flagship agricultural export, but the bigger money is not in exporting beans; it’s in processing.

What’s happening now (policy + market):

Ghana’s cabinet direction has reportedly moved toward allocating more beans to domestic processing and targeting at least 50% local processing from the 2026/27 season.

The market itself is volatile. Recent reporting highlights sector liquidity strains and reforms around pricing and financing structures.

On the global demand side, cocoa processing volumes (grindings) are a key indicator. ICCO estimates grindings at 4.81M tonnes (2023/24) and 4.60M tonnes (2024/25), a decline that signals demand softness and margin pressure for processors.

What this means for Ghana (the opportunity):

Ghana’s advantage isn’t only “good beans". It’s reliability + traceability + premium positioning, but that premium is maximised when Ghana exports the following:

cocoa liquor

cocoa butter (natural/deodorised)

cocoa powder (natural/alkalised)

cocoa cake / nibs

If the policy push toward higher processing is executed properly (not just announced), Ghana can grow:

industrial jobs

FX retention

technical capability (QA labs, food safety systems, certifications)

Styyer angle: buyers want consistency, documented specs, and risk-managed delivery; processing growth makes Ghana more of an “ingredient powerhouse", not just a bean origin.

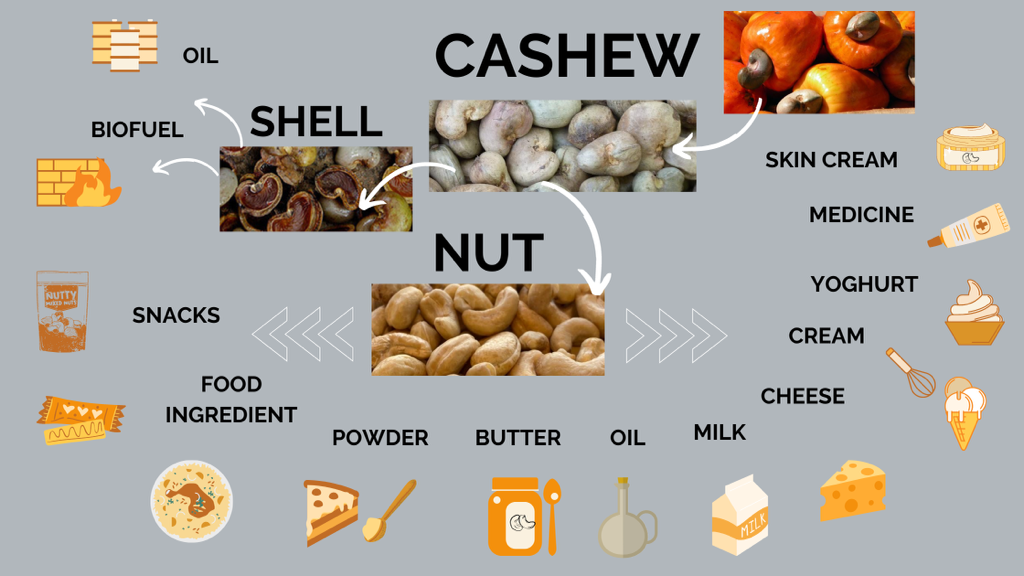

2) Cashew: Ghana can capture processing margin, if raw flows are properly managed

Cashew is one of the clearest “missed margin” stories in West Africa.

Ghana production signal:

One industry report estimated Ghana produced ~230,000 MT (2023) and then ~161,000 MT (2024) (a notable drop).

The real money is downstream:

The cashew kernel market is valued in the multi-billion USD range, with forecasts showing continued growth.

Regionally, processing momentum is accelerating: West Africa reportedly processed an estimated 732,000 tons into kernels in 2025 (up sharply year-on-year), showing that processing capacity is rising and competition is real.

Strategic problem (hard truth):

If raw cashew nut (RCN) flows are chaotic, smuggling, inconsistent farmgate pricing, and weak aggregation systems, processors can’t plan, factories under-run, and farmers get squeezed.

Strategic play for Ghana:

Better “raw management” first (the boring part that makes the money):

structured aggregation and grading

transparent farmgate pricing logic

moisture/quality controls at buying points

warehouse receipt systems / inventory finance

Then scale:

RCN → kernels

broken grades → industrial use

testa/shells → bioenergy / CNSL derivatives (where feasible)

Styyer angle: Styyer can position itself as the bridge between quality-controlled raw supply and export-grade kernels, backed by documentation and verified specs.

3) Oil Palm: Ghana consumes more than it produces; policy is moving toward expansion

Oil palm is often underestimated, but it’s a national balance-of-trade issue because edible oils influence food inflation and import bills.

Demand vs. supply gap signals:

A report citing Ghana’s domestic situation said annual palm oil consumption is about 250,000 MT, outstripping domestic production.

Ghana’s own oilseeds reporting (USDA/FAS) also tracks rising consumption patterns (e.g., palm oil’s role in food processing and household use).

Government direction:

Ghana’s finance ministry has publicly signalled policy work on oil palm expansion and a major job-creation agenda tied to economic crops like oil palm.

Additional reporting references a plan framed around large-scale investment (e.g., $500m) to boost the palm oil industry and reduce import dependence (treat this as directional, but still worth noting as a market signal).

Where the money is:

CPO (crude palm oil) is step one.

Refining/fractionation is where Ghana can seriously win:

RBD palm oil

olein/stearin fractions

specialty fats for food manufacturing

soaps & detergents base inputs

Styyer angle: a refined, documentation-led palm value chain (with traceability) is bankable and exportable, especially to industrial buyers.

4) Shea: global cosmetics demand is big; West Africa is moving to stop exporting raw value

Shea is one of Ghana’s most strategic “inclusive growth” commodities because it directly supports rural livelihoods, especially women-led activity across the chain.

Global market signal:

Ghanaian investment materials cite forecasts like a multi-billion-dollar shea butter market in the coming years (use them as directional market sizing rather than gospel).

Regional policy trend (very important):

Nigeria introduced a temporary ban on raw shea nut exports (time-bound) to push domestic processing, arguing the country supplies a huge share of raw nuts but captures a small slice of processed value.

That’s the playbook directionally: export less raw → process more domestically → capture margin.

What Ghana must get right (or it backfires):

Bans without industrial capacity = chaos.

The winning approach is the following:

secure raw supply for local processors through structured purchasing

invest in processing efficiency + quality systems

build export channels for refined butter and fractions.

Styyer angle: Styyer can publish spec-led shea content (moisture, FFA, insolubles, peroxide, micro) and position Ghana as a reliable origin for export-ready shea derivatives.

5) Soybeans: the quiet giant; protein demand keeps climbing (and Ghana’s feed sector is pulling)

Soy isn’t as glamorous as cocoa, but it’s brutally important because it underpins:

poultry feed

aquaculture feed

food manufacturing

protein ingredients

Ghana demand signal (credible numbers):

USDA/FAS forecasts Ghana’s soybean consumption around 215,000 MT (MY2023/24), up ~10% year-on-year, driven by food manufacturing, aquaculture, and poultry.

Ghana’s poultry sector reporting notes soybean meal can be imported freely and is a key feed input.

Global market context:

Soy markets are huge, and global supply is influenced by South American production cycles and price swings; oversupply/price weakness has been discussed for 2024–2025.

Where Ghana can win:

Not just grain trading and processing:

soybean meal (feed)

soybean oil (food/industrial)

texturised vegetable protein (longer-term)

The immediate opportunity is building predictable local supply for feed mills and processors, reducing import exposure.

Styyer angle: position soy as a “stability commodity” for industrial buyers, especially where buyers value documented origin and contract reliability.

The common thread: Ghana must manage the raw commodity better before scaling processing

Here’s the hard truth:

If Ghana doesn’t fix aggregation, grading, storage, traceability, and contract enforcement, then “processing ambitions” become expensive speeches.

The countries that win in commodities don’t just "produce"

They standardise.

That means:

tighter specs

fewer disputes

fewer rejections

consistent documentation

reliable shipment planning

FAQ

What are Ghana’s main agricultural exports?

Ghana’s main agricultural exports include cocoa, cashew nuts, palm oils, shea nuts, and soybeans.

Why is cocoa important to Ghana’s economy?

Cocoa is Ghana’s largest agricultural export and one of the world’s most important sources of cocoa beans for chocolate production.

Which African countries produce shea nuts?

The shea belt spans several West African countries, including Ghana, Burkina Faso, Nigeria and Côte d’Ivoire.

Ready to Lock In supplies?

If your business depends on:

✔ Stable pricing

✔ Quality assurance

✔ Proper documentation

✔ Predictable shipments

Then waiting is not a strategy.

Contact Styyer today and secure your Ghana supply pipeline.

👉 Submit your request: Product Inquiry Form

📩 sales@styyer.com